Ready to Buy?

Pack your bags, It’s time to turn those dreams into reality!

-

Your Trusted Real Estate Advisor:

With thousands of successful transactions under my belt, I’m dedicated to making your home-buying experience smooth and rewarding. I’ll leverage my expertise to:

- Find your dream home

- Negotiate the best deal

- Secure competitive mortgage rates

- Provide expert guidance and support

Let’s turn your homeownership dreams into reality.

Investor ROI Calculator

Paste a property link, enter assumptions, and get an instant ROI snapshot (cash flow, cap rate, mortgage + stress test).

Disclaimer: Estimates only. Mortgage “stress test” shown using OSFI minimum qualifying rate rule (greater of contract rate + 2% or 5.25%). Cap rate uses NOI ÷ property value.

1) Property & Lead Info

2) Financing

3) Income & Expenses

Note: This tool does not store data. If you want leads sent to Google Sheets/CRM, add a webhook URL in Settings → Nasim ROI Calculator.

ROI Snapshot

Summary (shareable)

—

Sources: OSFI stress test rule (contract rate + 2% or 5.25%): osfi-bsif.gc.ca • Cap rate definition: investopedia.com

Some of the buyer incentives/opportunities we offer our buyers include:

-

Unlock Your Homeownership Potential:

As our valued client, you’ll enjoy a range of exclusive benefits:

- Early Access: Be the first to know about upcoming power sales, distress sales, and foreclosures.

- Best Mortgage Options: Our expert mortgage brokers will help you find the perfect mortgage solution to suit your needs.

- Flexible Financing: We cater to diverse financial situations, offering solutions for self-employed individuals, new immigrants, and those with limited credit history.

- More Mortgage Options: Access to wide range of mortgage options, including A, B, and private lender financing, to cater to diverse financial situations. Whether you’re a first-time homebuyer or an experienced investor, we’ll find the perfect mortgage solution for you.

Mortgage 101

Mortgage Industry Jargon Explained

Baffled by some of the phrases realtors and bankers throw at you? Here are some commonly used—but not always understood—words to describe mortgages:

Amortization Period

This is the number of years it will take to repay the entire mortgage in full and is determined when you are approved. A longer amortization period will result in lower payments but more interest overall as it will take longer to pay off. The typical amortization range is 15 to 30 years.

Closed Mortgage

This is any mortgage where you have agreed to pay the lender for a specified period of time. This means that you cannot pay it off, refinance or renegotiate before the mortgage term ends without incurring a penalty. Depending on the lender, there may be options for accelerated payments but it depends on your particular mortgage contract. While these mortgages tend to be a lot stricter, they can often provide lower interest rates.

Conventional Mortgage

In the case of a conventional mortgage, the loan covers no more than 80% of the purchase price on the property. This means, the buyer has put 20% (or more) down on the property. These mortgages do not require default insurance due to the amount down.

Default

Failure to pay your mortgage on time will result in defaulting on the loan.

Derogs

Short for ‘derogatory’, derogs refers to an overdue account or late payments on your credit report.

Down

Short for down payment. In Canada, the minimum down payment is 5% on any home purchase.

Fixed

A fixed-rate mortgage means you are locked in at the interest rate agreed for a longer length of time.

Flex Down

This refers to a borrowed down payment program, which allows homeowners to “borrow” money for the down payment from a credit card, line of credit or other loan. In this case, the repayment of the loan is included in the debt calculations.

Foreclosure

This refers to the possession of a mortgaged property by the bank or lender if a borrower fails to keep up their mortgage payments.

High-Ratio Mortgage

A high-ratio mortgage is where the buyer has provided a down payment of less than 20% of the purchase price and needs to pay Canada Mortgage and Housing Corp. (CMHC) to insure the mortgage against default.

MIC

Short for a Mortgage Investment Corporation, this is a group of investors who will lend you the money for a mortgage if a traditional lender will not due to unusual circumstances.

Open Mortgage

An open mortgage means you can pay out the balance at any time, without incurring a penalty.

PIT

Principal, interest and taxes— a calculation representing the amount you can afford to pay monthly on your home. Heating costs are often included in this calculation (PITH).

Pull

Also known as a ‘credit check’ or ‘credit inquiry’ a ‘credit pull’ refers to the act of checking a credit report to determine if the borrower is a viable investment prior to approval of the mortgage.

Term

Term is the length of time that a mortgage agreement exists between you and the lender. Rates and payments vary with the length of the term. The most common term is a 5-year, but they can be anywhere from 1 to 10 years. Generally a longer term will come at a higher rate due to the added security.

Trade Lines

This refers to any credit cards, loans, wireless phone accounts, or mortgages that appear on your credit report.

Underwriting

This refers to the process of determining any risks relating to a particular loan and establishing suitable terms and conditions for that loan.

Variable

A variable-rate refers to an interest rate that is adjusted periodically to reflect market conditions.

20/20

A condition that refers to repaying 20% of the mortgage balance OR increasing your payment by 20%, without incurring a penalty.

The Mortgage Financing Process

The number one question for any potential homebuyer or someone new to the mortgage process is “what does this process entail?”. The following is a simple outline to give you an idea of the process and help you understand what to expect as you embark on your home buying journey!

STEP 1 – BE PREPARED

Having the following information on hand before meeting with your mortgage professional will help them determine what you qualify for and help them determine the best mortgage product for you:

- Contact information for your employer and your employment history

- Proof of address and your address history

- Government-issued photo ID with your current address

- Proof of income for your mortgage application

- Down payment proof (amount and source)

- Savings and investments proof

- Details of current debts and other financial obligations

STEP 2 – GET PRE-APPROVED

One of the best things any potential homeowner can do when starting the home buying process is to get pre-approved. Mortgage pre-approval requires submission and verification of your financial history and can help you determine your price range, understand the monthly mortgage payment associated with that price range and provide the mortgage rate for your first term.

It is important to note that pre-approval does not mean that a lender has fully reviewed your documentation and you may still need the approval of a mortgage insurer. However, it does have a lot of benefits that can give you a “leg-up” in your search!

BENEFITS OF PRE-APPROVAL

Getting pre-approved not only makes the search easier by helping to determine your price range and budget, but pre-approval also guarantees the interest rate for 90-120 days while you search for that perfect home. Plus, the rate will automatically be adjusted down with any market reductions. Another benefit to pre-approval is that, when it comes time to purchase, pre-approval lets the seller know that securing financing should not be an issue. This is extremely beneficial in competitive markets where lots of offers may be coming in.

Quick Tip: Being entirely candid with your home-buying team throughout the process will be vital! Hidden debt or buying a big-ticket item during your 90-120 day pre-approval can change the amount you are able to borrow. It is best to refrain from any major purchases (such as a new car) or life changes (such as changing jobs) until after closing and you have the keys to your new home!

STEP 3 – HIRE A REALTOR

In today’s competitive real estate market, it can be very difficult to acquire property WITHOUT the help of a realtor. One of the reasons realtors are integral to the home buying process is that they can provide access to properties that never even make it to the MLS website. Realtors also gain access to information about homes that may come onto the market before a listing is even signed.

Most importantly though, a realtor understands the ins-and-outs of the home buying process and can tell you how to be successful in your endeavors to purchase a home by guiding you through the process from the first viewing to having your bid accepted.

STEP 4 – SHOP THE MARKET & MAKE AN OFFER

Once you have found the property that meets your needs, you’ll put in an offer that’ll be accepted or countered. This may go back and forth until you reach an acceptable price with the vendor. To start home shopping today, check out the listings on SnapHomes.ca

STEP 5 – OFFER IS ACCEPTED

Once your offer is accepted with the condition of financing, you will need to do a few things to finalize the sale:

- Ask for a realtor intro between your mortgage professional and realtor.

- An appraisal may be required, which will be determined and arranged by your mortgage professional.

- Send in any remaining documents required for financing (income confirmation, down payment confirmation, etc).

- Arrange a home inspection.

- Receive the lender’s approval on property and final approval letter.

STEP 6 – REMOVE CONDITIONS

At this point, your financing is in place and you’re ready to proceed with the purchase of the property.

STEP 7 – LAWYER’S OFFICE

You’ll be asked to provide any money that’s to be used as your down payment, which is not already on deposit with your realtor. Typically, you’ll go in 1-2 days prior to the completion date.

3 Things You May Not Know About Cash-Back Mortgages

It can get pretty exciting to see campaigns around “cash-back mortgages” but, before you get too far along, here are three things you might not know about these types of mortgages:

1. Occasionally you will see campaigns on cash-back mortgages, so don’t jump at the first one you see! These types of mortgages are available through a few major lenders so it can be helpful to shop around to see what different terms and conditions are available, as this will affect the overall loan.

2. When it comes to cash-back mortgages, you’re really getting a loan on top of your mortgage. The interest rates are calculated to ensure that, by the end of your term, you will have paid the lender back the money they gave you (and perhaps a bit extra!). Be mindful that these loans can come with higher interest rates and, in some cases, the extra is more than you got in cash-back.

3. The average cash-back mortgage operates on a 5-year term. While you may not be planning to move before your term is up, sometimes things happen and it is important to be aware that if you break a cash-back mortgage, you have to pay the standard penalty but you will also have to pay back a portion of the loan you were given. For example, if you are 3 years into a 5-year term, you would have to pay back 2 years or 40% worth of the cash-back. Combined with the standard mortgage penalties for breaking your term, this can add up if you’re not careful!

Before signing for a cash-back mortgage it’s better to discuss your needs with your local mortgage expert. They can advise regarding all cash-back mortgage availability, lines of credit, purchase plus improvement loans or also flex down mortgages that may be better for your situation.

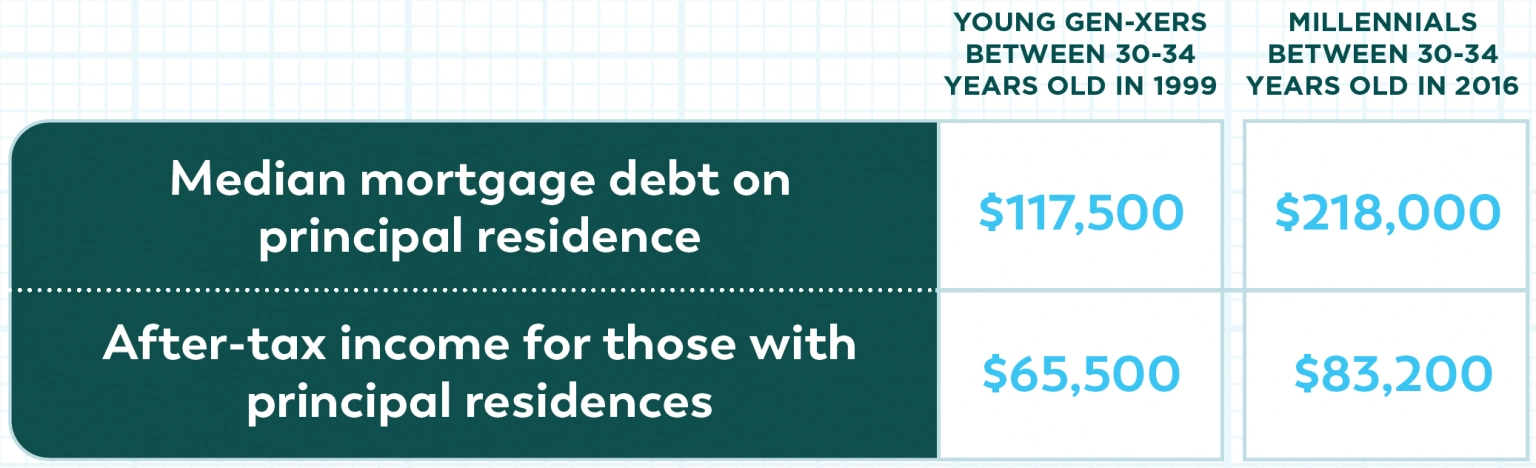

Millennials vs Gen X’ers.

Are millennials better or worse off than Gen-Xers at the same age?

Millennials are now the largest generation of people in Canada. They’re the most educated and diverse generation, but they face unique challenges…

- Millennials had higher after-tax household incomes than young Gen-Xers. Median after-tax household income between 25 and 34 years oldMillennials in 2016 $66,500

Young Gen-Xers in 1999 $51,000 - Millennials had higher assets and net worth than young Gen-Xers, but they also carried more debt.

Homeownership, living in Toronto or Vancouver, and having a higher education were three factors associated with higher net worth. - Millennials are relatively more indebted… Debt-to-after-tax income ratio

216% Millennials in 2016

125% Young Gen-Xers in 1999 - Though millennials are entering the housing market at similar rates as previous younger generations, they are taking on larger mortgages.

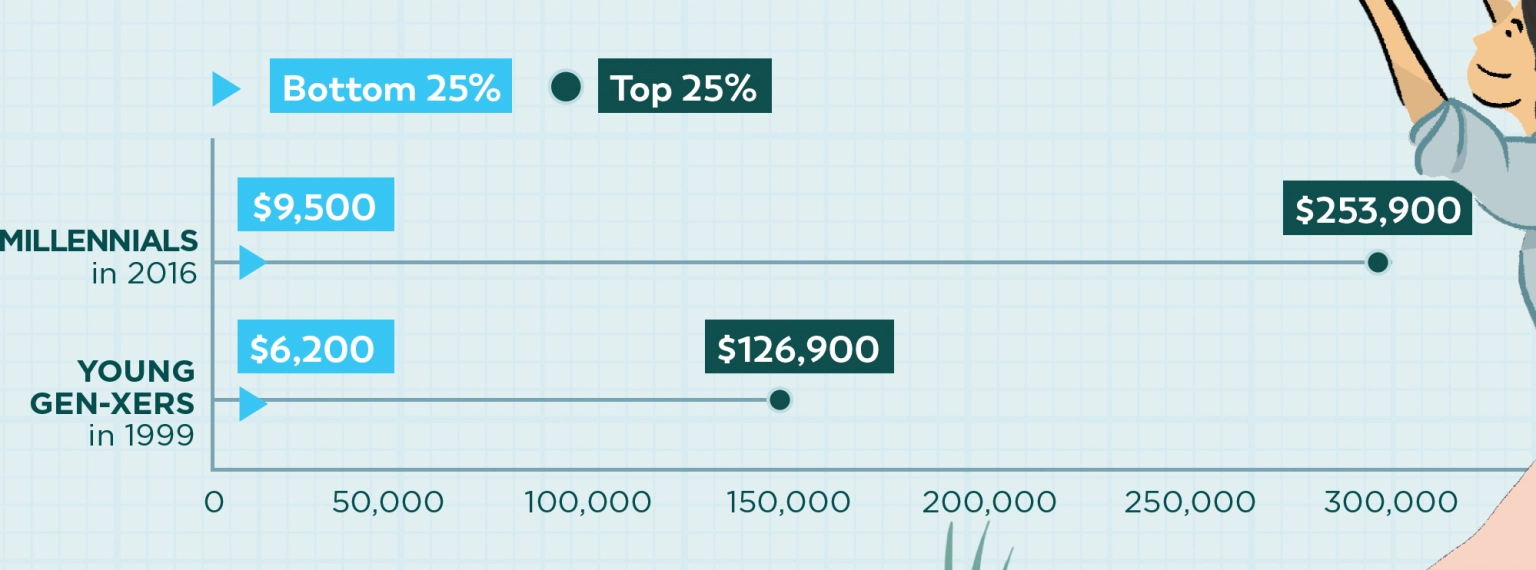

- Though their median net worth is higher, there are greater differences in economic well-being among millennials. Millennials in the top 10% held 55% of all total net worth accumulated by their generation.

Notes: Unless otherwise notes, millennials represent those between 25 and 34 years old in 2016, and young Gen X-ers indicate those between 25 and 34 years old in 1999.

Results are presented in 2016 current dollars and adjusted for inflation to allow a comparison over time. Statistics provided refer to the age and generation of the major income earner in the household or family.

ASSETS VS. LIABILITIES

Assets are what you own:

- Cash

- The value of your residence

- Artwork

- Automobile

- Checking account

- Collectibles

- Electronics

- Jewelry

- Investment accounts

- Retirement account

- Savings account

Liabilities are what you owe:

- Unsecured debts

- Car loan

- Mortgage

- Student loans

- Accounts payable

- Income taxes payable

- Bills payable

- Bank account overdrafts

- Accrued expenses

- Short-term loans

10 Mortgage Mistakes

Whether it is your first house or you’re moving to a new neighborhood, getting approved for a mortgage is exciting! However, even if you have been approved and are simply waiting to close, there are still some things to keep in mind to ensure your efforts are successful.

Many homeowners believe that if you have been approved for a mortgage, you are good to go. However, your lender or mortgage insurance provider will often run a final credit report before completion to ensure that nothing has changed. Changes in your credit usage and score could affect what you qualify for – or whether or not you get your mortgage at all.

To avoid having your mortgage approval status reversed or jeopardizing your financing, be sure to stay away from these 10 mortgage mistakes:

1. BEEFING UP YOUR APPLICATION

This is not a time to try and ‘beef up’ your financials; you must be honest on your mortgage application. This is especially true when seeking the advice of a mortgage professional, as their main goal is to assist you in your home buying journey. Providing accurate information surrounding your income, properties owned, debts, assets and your financial past is critical. If you have been through a foreclosure, bankruptcy or consumer proposal, disclose this right away as well. We are here to help!

2. GETTING PRE-APPROVED

With all the changes and qualifying requirements surrounding mortgages, it is a mistake to assume that you will be approved. Many things can influence whether or not you qualify for financing such as unknown changes to your credit report, mortgage product updates or rate changes. Getting pre-approved is the first step to ensuring you are on the right track and securing that mortgage! Most banks consider pre-approval to be valid for four months. So, even if you aren’t house-hunting tomorrow, getting pre-approved NOW will come in handy if a new home is in your near future.

3. SHOPPING AROUND

One of the biggest mistakes people make when signing for a mortgage is not shopping around. It is easy to simply sign up with your existing bank, but you could be paying thousands more than you need to, without even knowing it! This is where a mortgage broker can help! With access to hundreds of lenders and financial institutions, a mortgage professional can help you find a mortgage with the best rate and terms to suit YOUR needs.

4. NOT SAVING FOR A DOWN PAYMENT

Your down payment is a critical part of homeownership and a useful financial tool that you should utilize when purchasing a home. A down payment reduces the overall amount of financing you need and increases the amount of equity right from the start. Down payments also show the bank you are serious. In Canada, the minimum down payment is 5% (with mortgage insurance), with the recommended being 20% if possible.

5. CHANGING EMPLOYERS OR JOBS

As employment is one of the most important factors that determines whether or not you qualify for financing, it is important not to change employers if you are in the middle of the approval process. Banks prefer to see a long tenure with your employer, as it indicates financial stability. It is best to wait for any major career changes until after your mortgage has been approved and you have the keys to your new home!

6. APPLYING OR CO-SIGNING FOR OTHER LOANS

Applying for additional loans or financing while you are currently in the midst of finalizing a mortgage contract can drastically affect what you qualify for – it can even jeopardize your credit rating! Save any big purchases, such as a new car, until after your mortgage has been finalized.

Also, just as applying for new loans can wreak havoc on a mortgage application, so can co-signing for other loans. Co-signing signifies that you can handle the full responsibility of the debt if the other individual defaults. As a result, this will show up on your credit report and can become a liability on your application, potentially lowering your borrowing power.

7. AVOIDING CREDIT MISSTEPS

As mortgage financing is contingent on your credit score and your current debt, it is important to keep these things healthy during the course of mortgage approval. Do not go over any limits on your cards or lines of credit, or miss any payment dates during the time your finances are being reviewed. This will affect whether or not the lender sees you as a responsible borrower.

Also, although you might think an application with less debt available to use would be something a bank would favor, credit scores actually increase the longer a card is open and in good standing. Having unused available credit and cards open for a long duration with a good history of repayment is a good thing! In fact, if you lower the level of your available credit (especially in the midst of an application) it could lower your credit score.

8. HAVING TOO MUCH DEBT

Credit card debt is on the rise and overuse of lines of credit can put you at risk for debt overload. Large purchases such as new truck or boat can push your total debt servicing ratio over the limit (how much you owe versus how much you make), making it impossible to receive financing. Some homeowners have so much consumer debt that they aren’t even able to refinance their home to consolidate that debt. Before you start considering a new home, make sure your current debt is under control.

9. LARGE DEPOSITS

Just as now is not the time for new loans, it is also not the time for large deposits or “mattress money” to come into your account. The bank requires a three-month history of all down payments and funds for the mortgage when purchasing property. Any deposits outside of your employment or pension income will need to be verified with a paper trail – such as a bill of sale for a vehicle, or income tax credit receipts. Unexplained deposits can delay your mortgage financing, or put it in jeopardy if they cannot be explained.

10. MARRYING INTO POOR CREDIT

Having the financial talk before getting hitched continues to be critical for your financial future. Your partner’s credit can affect your ability to get approved for a mortgage. If there are unexpected financial issues with your partner’s credit history, make sure to have a discussion with your mortgage broker before you start shopping for a new home.

If you are currently in the midst of a mortgage application, or are looking to start the process, don’t hesitate to reach out to us today to ensure that you do things the RIGHT way to succeed with your home purchase.

Contact us

Thank you for getting in touch! Please complete the form below, and our team will respond promptly. We’re here to help with all your real estate needs!